OLED: 2017 breakthrough soon, three years of 300 billion Capex, spawned 70 billion equipment market space. A customer leads, smart phone is expected to fully introduce OLED in 2017, which will cause the industry to erupt, and the trillion display market has huge space for a long time. At present, the production capacity of Samsung's 160,000 pieces/month is only enough for “self-use + 100 million new machines for A customers next yearâ€. Other Android camp mobile phone manufacturers face “one screen is hard to findâ€, which forces panel manufacturers to accelerate production expansion. Including Samsung, LG, BOE, etc. In the next three years, panel manufacturers have announced plans to expand their production by more than 300 billion yuan, 80% of which will be invested in equipment, which will generate 70 billion yuan of equipment market space per year. It is expected that the market space of the front, middle and rear equipment will be 500/120/10 billion yuan respectively.

Front equipment: LTPS is the trend, laser equipment is the most flexible. Due to its ability to meet high current requirements, LTPS is the mainstream technology for OLEDs. The market space for front-end equipment is 50 billion yuan per year. Under the LTPS technology flow, laser equipment is the most flexible, and the market space is expected to be 20 billion yuan per year in 2017-2019. Orders for laser device leader Coherent skyrocketed. In the second quarter of 2016, orders for microelectronics reached US$367 million, an increase of 248.8% year-on-year, of which OLED accounted for more than 80%, confirming the explosion of the industry. In terms of domestic manufacturers, Dazu Laser has benefited a lot. At present, OLED 80% laser processing equipment has been laid out. It is expected to gradually reach production in 2017-2018, and it is expected to contribute more than RMB 1 billion in revenue in 2018.

Middle equipment: The demand for evaporation equipment is in short supply, and it is urgent to break through the capacity bottleneck. The middle process includes evaporation and packaging, and the market space is about 12 billion yuan per year. Evaporation is used to make luminescent materials, which is the core of the entire OLED process and the key to controlling the yield of OLED panels. Therefore, the middle road is a window to observe the expansion process of the entire industry. At present, more than 85% of the evaporation equipment on the market comes from Canon Tokki, Japan, and 90% of its production capacity was taken over by Samsung in 2017, resulting in “one machine is hard to findâ€. The evaporation equipment has become the key to restrict panel manufacturers to expand OLED production capacity. Where. The packaging equipment led by Jusung Engineering of Korea, a core supplier of Samsung and LGD, with an order of 823 million yuan in 2016, a year-on-year increase of 141%, confirming the outbreak of the industry.

After the equipment: non-standard automation, domestically replaced the main battlefield. The latter process includes “cutting + bonding + Bonding + detectionâ€, all of which are non-standard automation. The product replacement equipment is replaced, and the update frequency is almost every 2 years. Therefore, the equipment manufacturers are required to support and respond quickly, and domestic manufacturers benefit. The annual market space of the downstream equipment is 10 billion yuan, of which the “fit + Bonding+ test†7 billion market space is calculated according to the 25% net interest rate of non-standard automation equipment. We believe that the profit of the whole industry is about 1.8 billion, if the leading company can Taking away 30% of the profits of the whole industry, it is expected to generate listed companies with a market value of around 15 billion.

Risk factors: The capacity and yield of evaporation equipment are not up to expectations; the demand for downstream smartphones is slowing; the competition in the equipment manufacturing industry is intensifying.

Investment Strategy. OLED outbreaks, Capex first, equipment benefits. It is estimated that the market space of the front/middle/rear equipment will be 500/120/10 billion yuan. The laser equipment under the LTPS process is the most flexible, with an annual increase of 20 billion laser equipment. Zhongdao is the observation industry window, paying attention to the progress of core evaporation equipment expansion and the improvement of yield. After the non-standard automation, domestically replaced the main battlefield. For the first time, it gave the OLED equipment industry a “Outperform†rating. In terms of targets, we will focus on recommending the most flexible lasers in the industry, and benefiting from the outbreak of OLED explosions. At the same time, we will focus on the related listed companies on the main battlefields, including Zhiyun, Lianhe, Jingzheng, and New. Sanban Company Shenkeda.

Industry Overview: OLED will replace LCD as the mainstream display technology

OLED is the core of third-generation display technology. Display technology is the most important way for humans to obtain information. The global market space is nearly one trillion yuan. The revolution of each generation of display technology will cause great changes in downstream terminals. In 1897, CRT (Cathode Ray Tube) was invented, and then its most important application was the birth of television. Humans entered the era of image display. In the 1990s, the second-generation display technology represented by PDP (plasma) and LCD (liquid crystal) developed rapidly. Due to the thin and light advantages of LCD, portable display application terminals represented by mobile phones and notebook computers were realized. As the third-generation display technology, OLED's core competitiveness is thinner and more flexible, which is expected to open the door to the era of flexible display.

Three advantages help OLEDs replace LCDs. Compared to LCDs, OLED displays have three major advantages:

First, it is lighter and thinner without a backlight. The LCD itself cannot emit light, and adopts LED as its backlight. Its structure from bottom to top includes: backlight layer, polarizer, TFT substrate, liquid crystal layer, color filter and second polarizer; OLED emits light itself, no need for LCD In the backlight layer and the liquid crystal layer, the number of polarizers is also reduced, so that the structure is simpler, lighter and thinner, and the thickness is only 0.4 mm, which is less than half of that of the TFT-LCD.

Second, the all-solid structure is highly reliable and bendable. The OLED device is an all-solid-state mechanism, free of vacuum and liquid substances, and is superior in shock resistance to LCD devices, and can be fabricated on a flexible material substrate, thereby enabling flexible display.

Third, the color gamut has a wide viewing angle and a fast response, and is suitable for the needs of wearable devices. Wide range of color gamut: OLED's NTSC standard color gamut can reach 110%, while LCD is only 70%~90%; wide viewing angle: OLED self-illumination makes viewing angle up to 170 degrees; faster response: OLED display The response speed is far faster than the LCD screen. There is no tailing when displaying the dynamic picture, which can obviously reduce the blur phenomenon of the playback motion picture, and is more suitable for VR display to prevent vertigo.

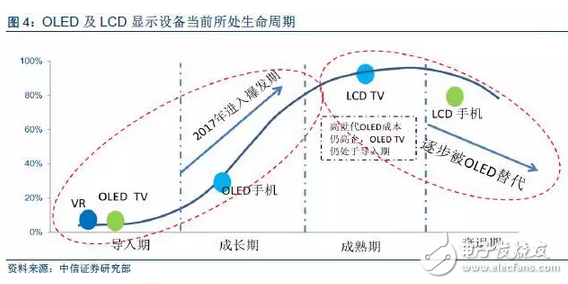

The two driving forces look at the OLED industry to determine the outbreak in 2017. First, the vision space. Show the industry trillion market space. AMOLED mobile phones entered the growth phase in 2017, and the penetration rate is expected to increase from 10% to 40% in the next three years. After 2019, the TV panel is expected to relay, providing long-term driving force in the industry. According to IHS data, the area of ​​panels consumed by global mobile phone screens only accounts for about 6% of the total panel sales area. In the future, the production cost of large-size OLED panels will decrease, and the penetration of OLED TVs will deepen, which will be more than 10 times that of mobile phones.

Second, the recent catalysis. A customer has a high probability of introducing 100 million OLED phones in 2017, and Android manufacturers are expected to follow up. At present, the production capacity of Samsung's 160,000 pieces/month is only enough for “self-use + 100 million new machines for A customers next yearâ€. Other Android camp mobile phone manufacturers face a hard-to-find situation, which forces panel manufacturers to accelerate production expansion. Including Samsung, LG, BOE, etc. In the next three years, panel manufacturers have announced plans to expand their production by more than 300 billion yuan, 80% of which will be invested in equipment, which will generate 70 billion yuan of equipment market space per year.

Industry's core drivers: OLED outbreaks, Capex pioneering equipment benefits the most

Vision-driven: entering the growth period in 2017, looking at the trillion market in the long run, spurring billions of equipment investment

The short-term development momentum of AMOLED is mainly due to the deepening of smartphone penetration. Nearly 90% of AMOLED market demand comes from smartphones. The AMOLED panel market in 2016 was $15 billion, an increase of approximately 25% from the $12 billion in 2015. The AMOLED market is expected to reach US$28 billion by the end of 2020, with a compound annual growth rate of approximately 17.6%. In the long run, the small-screen increment of OLED TV with small and medium-sized OLED curved screen brought by VR is expected to relay smart phones and continue to provide powerful kinetic energy for OLED development.

TVs have a lot of kinetic energy, or relay phones provide the driving force for OLEDs. In the large-size TV screen application, the cost is the main obstacle to the promotion of OLED. Taking a 55-inch UHD panel as an example, according to IHS data, the average LCD price is about $210, while the OLED production cost is only $700. The cost gap between the two is estimated to be as high as 200%. In the future, inkjet printing instead of evaporation will significantly reduce the cost of large-size OLED production. OLED inkjet printing simplifies the process by spraying the coating material on the substrate without the need for expensive and complicated procedures. This technology is expected to significantly reduce the cost of OLED production. According to IHS data, the area of ​​panels consumed by global mobile phone screens only accounts for about 6% of the total panel sales area. In the future, the production cost of large-size OLED panels will decrease, and the penetration of OLED TVs will deepen. The corresponding market size will be more than 10 times that of mobile phones.

OLED is an inevitable choice for VR. The four advantages determine the preferred AMOLED for VR display: First, the response time is short and the refresh rate is high: it is beneficial to solve the problem of VR “dizzinessâ€. The OLED response time is less than 1 microsecond, while the LCD is typically about 10 milliseconds. Second, the wider field of view enhances VR immersion. The VR immersion is determined by the user's actual field of view. The OLED viewing angle is up to 170°, which is higher than the LCD's 120°. Third, lower power consumption and increased VR standby time. Fourth, the quality is lighter: Since the VR is worn on the head, the lighter the quality, the better the user experience.

The third-generation display technology leader, long-term look at the market space of trillions, spurs billions of equipment investment. According to IHS's latest forecast, the global display panel market space in 2016 is as high as $132 billion, of which OLEDs account for only 10%. In the future, with the full penetration of OLEDs in the display field, and the growth of emerging application markets such as VR, the market space that may penetrate in the long run is as high as RMB 10,000 billion. However, in the field of large-size display, it is also facing competition from new technologies such as laser display. The trillion market space will drive 300 billion Capex in the next three years, 80% of which will be invested in the equipment field.

Recent Catalysis: A customer introduction, the industry is in short supply, accelerating equipment investment

A customer or import OLED smartphone in 2017. According to Display Research, in 2017, the top international consumer electronics company A is expected to introduce OLED screens for the first time in a new iPhone, which will drive the new round of consumer electronics upgrades. On October 26, 2016, Company A disclosed the FY2016 annual report showing a nearly one-billion-dollar purchase order over one-year, combined with the emerging key components of the off-balance sheet purchase obligation and risk alert disclosed in its three quarterly reports. Procurement risk, this $4 billion is likely to be a long-term supply contract for AMOLED screens issued to Samsung. On February 13, 2017, according to The Investor website, Samsung Electronics' Samsung Display Company and A customer reached a new agreement to supply an additional 60 million OLED panels for the next generation of iPhone, worth 5 trillion won (about 43 One hundred million U.S. dollars).

Android camp: Samsung led, domestic mobile phone manufacturers to quickly follow up. Samsung is currently the largest manufacturer and user of AMOLED displays. According to DIGITIMES Research, AMOLED penetration has reached 70% in all of Samsung's 320 million smartphones in 2015. The entire AMOLED display capacity of AMOLED is only 470 million pieces in 2017, which can only support the demand of Samsung Galaxy series and A customers in 2017, so domestic manufacturers are facing tight production capacity or even unable to get goods. Expansion of production increases equipment investment.

OLED screens may become the most scarce electronic components in 2017, and domestic mobile phones may face out of stock. As one of the most important innovations in the smartphone market in 2017, OLED screen is expected to become a very important competitive point for domestic high-end smartphones. According to our incomplete statistics, the main models of domestic mobile phone manufacturers that have already planned to import AMOLED screens include Huawei's Mate9 Pro, OPPO's R9s, VIVO's Xplay5, Xiaomi's Note2, Jinli's M6, etc. We assume these main machines All models use AMOLED screens, and their demand is as high as 80 million pieces. Compared with the current supply capacity of Samsung, it is almost inevitable to face shortage.

The tight production capacity will continue until 2019, and the drive panel manufacturers will accelerate production expansion. Based on the OLED investment plans of major panel manufacturers at home and abroad, we estimate that the global small and medium-sized OLED production capacity in 2017/2018/2019 will be 320/520/7 million pieces/year (using 1,500x1,850mm glass substrates in the 6th generation line). The number of calculations). According to the aforementioned demand data, the sales volume of global flexible OLED mobile phones in 2017/2018/2019 reached 4.3/5.75/654 million units, and the screen availability rate was 200%, which made the global demand for flexible OLED screens up to 8.6/11.5/12.9. Billion tablets. According to the 5.5-inch screen, the OLED capacity demand for 2017-2019 is 428/573/646 million pieces/year. Based on the above calculations, we judge that the global OLED market will be the seller's market in 2017 and 2018. The capacity gap will exceed 20% in 2017 and 10% in 2018. The huge capacity gap will drive the industry to rise in volume and price in 2017, and such a tight situation will also drive OLED panel makers to accelerate investment expansion.

Industry market space: 300 billion Capex for three years, spawning 70 billion equipment market

In the next three years, the total investment in OLED plans of panel makers at home and abroad will exceed 300 billion. In response to the outbreak of downstream demand, domestic and foreign large manufacturers have increased their investment in OLEDs, especially in the field of small and medium-sized OLED panels. For domestic manufacturers, BOE's OLED investment plan for the next three years will be as high as RMB 73 billion. The mainland's investment plans including Shenzhen Tianma, TCL, Huiguang and Kunshan Guoxian have reached 200 billion yuan; In terms of factories, Samsung, LGD, Sharp and other total investment in 2017 reached 7.4 billion US dollars, equivalent to about 50 billion yuan.

Production line investment is still dominated by small-sized smart terminal screens. Due to the current lack of price competitiveness of OLED TVs, only South Korean panel makers LGD and Samsung have a clear expansion plan. For example, Samsung and LGD plan to invest about 20 billion yuan to build the 8th generation AMOLED production line. Most other panel makers are very cautious about the AMOLED high-generation line expansion plan, and the small and medium-sized production line expansion plan has already taken practical action to compete for expansion.

Three-year investment of 300 billion yuan has spawned a market of 210 billion upstream equipment. In 2016, the global major panel makers' AMOLED investment plans totaled over RMB 320 billion. The production time of the AMOLED production line of various manufacturers and the conversion or new production line plan will be calculated. The investment of 320 billion yuan will bring about 200 billion yuan of equipment demand and will be gradually released in the three years of 2016-2018.

Industry investment logic: the three major sub-sectors, the front is the most flexible, the latter domestically replaced the main battlefield

The front/medium/rear equipment market will benefit. OLED devices are divided into front-end equipment (based on LTPS laser crystallization, semiconductor lithography, etch deposition equipment), medium-channel equipment (evaporation + packaging), and downstream equipment (Bonding + bonding + testing). According to UBI, the market space of pre/middle/rear equipment is 69%/17%/14%, corresponding to the equipment market space of approximately 1450/360/294 billion in 2016-2018.

The middle road determines the production capacity and focuses on the investment opportunities before and after. Our core judgments on these three equipment markets are: front equipment, LTPS dominated, laser equipment is the most flexible; middle equipment, evaporation is Canon Tokki monopoly, urgent need to expand production to break through industry bottlenecks; rear equipment, module assembly automation , Bonding + fit + test, customized demand to promote the domestic alternative battlefield.

Front equipment: LTPS dominates, laser equipment deep benefits

Market space: LTPS front channel equipment market space of 50 billion yuan

OLED front-end process: making backplanes, led by LTPS technology. The main function of the backplane for the display panel is the underlying support and the drive electrodes. The OLED panel adopts an organic electric light-emitting diode as a display unit, and the current drives the organic semiconductor material and the luminescent material to emit light, and the size of the current is controlled by the TFT switch to determine the illuminating brightness. Unlike an LCD panel that drives liquid crystal molecules to rotate by voltage control to control the amount of transmitted light, the OLED panel requires a relatively large current flow of the underlying electrode. The electron mobility rate in low temperature polysilicon (LTPS) is 200-300 times faster than that of amorphous silicon (a-Si), which can provide more current, faster reaction speed and better stability. It is the main backplane driver used in AMOLED. technology.

LTPS is not proprietary to OLEDs, and high-end small-screen TFT-LCDs are also used, with a current penetration rate of 30%. Due to its fast response and power saving advantages, LTPS has also been adopted in high-end small-screen TFT-LCDs for mobile terminals. For a long time in the past, the global LTPS production capacity was basically covered by the iPhone of major customers. The main suppliers include Japan Display (JDI), LG Display (LGD) and Sharp. The remaining capacity is applied by other mobile phone manufacturers in high-end models. However, as the competition in the mobile phone market becomes more and more fierce, JDI, LGD and Sharp are also beginning to pay more and more attention to mainland brand terminals. At the same time, since 2016, there have been many LTPS production lines in the world, including the 6th generation LTPS production line of Huaxing Optoelectronics and the 6th generation LTPS production line of Xiamen Tianma. The 6th generation of the factory in Kunming Road and Kaohsiung Road LTPS production line, new capacity of AUK Kunshan's 6th generation LTPS plant. The release of these capacities has enabled LTPS to exceed 30% in TFT-LCD applications in 2016. By 2019, the market for smartphone screens based on LTPS-based LCDs and AMOLEDs is expected to be close to 70%.

In the next three years, the market space of the former LTPS equipment will reach 50 billion yuan per year. According to UBI's calculations, the total proportion of front-end equipment in AMOLED processing equipment is as high as 70%, which is the largest market for AMOLEDs. The market space in the next three years is as high as 50 billion yuan/year. In LCD panels with LTPS technology, the cost of the front LTPS devices is as high as 50%.

Investment logic: Laser equipment is the most flexible, is the core increment of LTPS front process

Laser equipment is the core increase in the LTPS process. From the manufacturing process of LTPS, it mainly includes buffer layer active layer growth (mainly using PECVD and cleaning equipment), polysilicon crystallization (mainly using laser crystallization equipment), 12-channel lithography + ion implantation (mainly using lithography machine, Etching machine, ion implanter, washing machine, laser plate making equipment) three-part process. Among them, lithography machine, etching machine PECVD and other equipment will also be used in the traditional α-Si TFT-LCD production line, equipment can be shared and migrated; while the ion implanter is an incremental device, but in the field of integrated circuits The amount is much larger than in the field of display devices, so the equipment is not flexible. The most flexible device in the entire LTPS process is the laser crystallization device.

Among the OLED front and rear equipments, the laser equipment is also very flexible. It is estimated that the annual market space will be 20 billion yuan in the next three years. In the front LTPS process, laser processing can be used in addition to the crystallization process (generally a high-power laser with a power of more than 1kw), including laser plate making that is widely used in 12-pass lithography processes (generally Medium power laser CO2 laser between 100w and 500w), direct semiconductor laser for heat treatment, and DPSS and excimer laser for ablation. In addition, laser equipment, including contact holes, touch screens and light guides for laser plate making, OLED screen cutting (CO2 laser, short-wavelength UV semiconductor pumped solid state (DPSS)) are also used in the middle and back processes. Laser and picosecond lasers, as well as laser stripping equipment used in flexible displays. We estimate that the laser process used in the entire OLED processing is about 12 channels, and the corresponding equipment investment will reach 20 billion yuan per year for the next three years.

Competitive landscape: US manufacturers control core devices, equipment, Japanese and Korean manufacturers dominate

The core devices are controlled by US vendors and will benefit in depth from OLED outbreaks. Coherent Inc. is a leading supplier of excimer lasers and UV optical systems. Its main products downstream involve all laser OLED processing including laser crystallization, laser stripping, cutting, plate making, etc. Linebeam products with a maximum laser power of more than 1 kW are widely used in the manufacture of LTPS substrates. Benefiting from the expansion of OLED production capacity of China, Japan and Korea panel production, the company's microelectronics manufacturing equipment business added 367 million US dollars in the second quarter, of which OLED equipment new orders exceeded 300 million US dollars, accounting for more than 80%. New orders from China, Japan and South Korea include Linebeam 1000, Linebeam 1500 and UV Blade systems.

Benefiting from the outbreak of OLED equipment, orders from related companies have surged, and revenue growth is expected to exceed 150%. In FY2015, related companies had revenues of US$ 818 million, of which microelectronics accounted for more than 51%. In the second quarter of 2016, the company's new orders reached US$496 million, an increase of 81.8% from the previous quarter and an increase of 125.1% from the same period last year. Orders in the microelectronics segment reached US$367 million, accounting for approximately 74%, an increase of 94.7% from the previous quarter and an increase of 248.8% from the same period last year. In the microelectronics segment, OLED equipment orders contributed the most, exceeding $300 million. The performance of the coherent company also confirmed the eve of the OLED outbreak, equipment companies have begun to explode.

Japan and South Korea manufacturers to control equipment OLED laser processing equipment, domestic manufacturers look at the Han family laser, is expected to benefit from the OLED outbreak. Dazu Laser has been able to achieve the self-made of small and medium-power laser light sources. In the high-power field, it is necessary to purchase coherent and IPG light sources to manufacture laser equipment, so it is competing with related companies. At present, in the laser processing of OLED, the company has arranged about 10 developments. It is expected that there will be 2 mass productions in 2017, and the rest will break out in 2018. We expect the company's OLED laser equipment revenue to increase rapidly, reaching 1 billion yuan by 2018, becoming an important increase for the company.

Middle equipment: evaporation equipment is in short supply, and it is urgent to break through the capacity bottleneck

Market space: mainly based on evaporation coating, market space exceeds 10 billion

The OLED mid-range process is vapor deposition and packaging, and the market space is expected to be approximately RMB 12 billion per year. The organic light-emitting layer, the hole transport injection layer, the electron transport injection layer and the metal electrode on the current ITO glass of the AMOLED panel are all realized by vapor deposition coating.

The alignment accuracy of vapor deposition is a major difficulty in the process. At present, there are still problems such as insufficient yield and waste of organic materials, which is the key to the insufficient yield of the entire OLED panel. Therefore, it is also the core and most scarce equipment in the OLED production line. one. In addition, AMOLED organic light-emitting materials and metal electrodes are highly susceptible to moisture oxidation due to moisture from external and internal materials. In order to ensure the stability and longevity of the display panel, it is necessary to encapsulate the ITO glass on which the luminescent layer and the electrode are vapor-deposited in an inert gas atmosphere, and to fill the cover plate with water, metal, flexible polymer, film, etc. material. The market space for the entire evaporation and packaging equipment is around RMB 12 billion per year.

Investment logic: Titanium evaporation equipment is tight, limiting the capacity expansion of OLED industry chain

At present, only one of Canon Tokki's high-quality suppliers is available, and Samsung monopolizes 90% of its production capacity in 2017, which makes it difficult to find a “machineâ€. At present, Tokki, a subsidiary of Japan's Canon, is recognized as the best in vapor deposition equipment. The only manufacturers in the world with large-scale mass production performance are the Tokki family. Therefore, Tokki basically monopolizes the supply of global vapor deposition machines. Since Canon Tokki's 90% of its production capacity in 2017 was packaged by Samsung, other manufacturers had to consider cooperating with new evaporating suppliers. For example, Xinli spent 51.9 billion won to purchase SFA's evaporation equipment. A large number of OLED production results, because the evaporation process itself is the key to the OLED yield, the use of equipment from the new evaporation equipment manufacturers, resulting in OLED mass production yield is more uncertain.

Evaporation equipment is the key bottleneck in the industry and the key to affecting yield and productivity. The core luminescent materials of small and medium-sized OLEDs are currently produced by evaporation technology. The evaporation is the lowest yield in the whole process, so it directly determines the yield of the panel.

At the same time, manufacturers of high-volume and stable mass production of vapor deposition equipment are currently only available to the Canon Tokki family, which will limit the capacity of the entire industry.

The penetration trend of flexible displays determines the future of film packaging. The thin film package is characterized by the effective use of materials in the event of large bending deformation. In order to obtain a flexible organic display or other electronic equipment, the front and rear substrates must have sufficient flexibility to effectively isolate moisture and oxygen. The film package not only meets the requirements of folding and bending, but also has a certain strength to ensure the practical application requirements of the product. Therefore, we believe that the film package will become the mainstream in the future.

Competition pattern: Canon Tokki is big, and supply is in short supply and is expected to last until 2018

“Expansion + new supplier introductionâ€, the supply shortage is expected to be 2018 or eased. At present, only one manufacturer of the vapor deposition equipment capable of mass production and stable mass production is the Canon Tokki family. Other manufacturers have expanded the key evaporation equipment to ease the supply shortage. The vapor-coated reticle giant Japan Printing (JNP) announced that it plans to invest 320 million yuan by 2020 to increase the production capacity of vapor-deposited reticle by adding a production line for the production of OLED panels, which is indispensable for the production of OLED panels. Up to 3 times the current level. Canon Tokki said it plans to double the capacity of OLED panel equipment and expand the capacity of several partner companies. In addition, Korean companies have gradually entered the market of vapor deposition equipment. LGD has cooperated with Sunic System, a local small and medium-sized enterprise in South Korea, to develop evaporation equipment. It has signed large-scale supply orders with Sunc System and YAS to gradually increase the localization rate of production lines to over 50%.

Korea's Jusung Engineering leads the packaging equipment supplier, and the OLED business has the greatest growth flexibility. South Korea's JusungEngineering is the sole supplier of LGD from large to small packaging equipment and is Samsung's main supplier. In the display segment business, the company's 2015 revenue was equivalent to approximately RMB 340 million, of which LCD and OLED each accounted for half. The company expects orders in 2016 to be equivalent to RMB 823 million, an increase of 141% year-on-year. Among them, OLED equipment revenue will account for 80% of total revenue, and LCD will account for 20%, verifying the outbreak of OLED equipment industry.

After-channel equipment: non-standard automation, domestically replaced main battlefield

Market space: domestically replaced main battlefield, tens of billions of market space

Cutting + fitting + Bonding + detection, non-standard automation, high frequency of equipment update. After the assembly process of the AMOLED module, the OLED panel that has been vapor-deposited is first cut into the required size of the actual product and tested. Next, the polarizer is attached, and the chip and the flexible circuit board are Bonded to the display panel, the PCB board is pasted and connected to the panel, and then the AMOLED panel is attached to the cover with the touch sensor. Perform module aging test and lighting detection. The entire process will use 3-5 times of bonding and Bonding. Different from the standardized process flow of the display panel, the process of the panel module is generally highly customized, and the main factor module generally involves non-standardized designs such as routing and layout, which are different due to changes in the internal structural design of the mobile phone, which also leads to The automation equipment for OLED modules is also highly customizable. Although compared with the TFT backplane production and evaporation packaging equipment, the module assembly equipment purchase amount is relatively small, but due to its highly customized characteristics, the equipment has a short service life, frequent replacement and frequent market growth. The customized equipment is upgraded with the screen, and the replacement cycle is about two years. The market space of the entire “Cut + Fit + Bonding+ Detection†equipment is about RMB 10 billion per year.

Investment logic: leading customers, module automation acceleration, spawning billions of companies

A customer leads, 2017 capital expenditure drives the rapid growth of OLED module automation. In the FY16 annual report, A customers expect 2017 capital expenditures to rise significantly to $16 billion to develop the next generation of new iPhones. If we import OLED screens, we estimate that the proportion of the screen's total machine cost will rise to more than 20%. Company A is bound to increase the capital expenditure of automated assembly of OLED screens to ensure its yield. The growth of the module automation market is expected to accelerate.

Competitive landscape: the rapid rise of customized domestic equipment, spurring billions of market capitalization companies

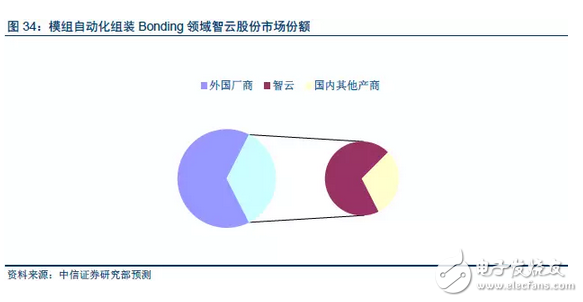

Japanese companies occupy the high-end market, and customized domestic equipment is rapidly emerging. 5-6 Japanese companies such as TEL, Panasonic and TEK are the world's leading LCM automated assembly and testing equipment. As the current global 3C manufacturing assembly line continues to shift to mainland China, China's non-standard automation company can provide customers with the advantage of geographical advantage and engineer dividends, and meet the customer's customized rapid development requirements of about 2 months, so it will rise rapidly and gradually Replace Japanese suppliers. Local non-standard automation vendors, including Zhiyun, Liande, Shenkeda, Zhengye Technology, and Taiyuan Fenghua, are rapidly emerging.

The market for flexible AMOLED module equipment is expected to reach 6.19 billion yuan in 17 years. Due to the high degree of customization of the OLED screen rear-end module equipment, the OLED panel technology has a large change relative to the LCD screen, so the OLED module equipment market will usher in an explosion. We assume that a touch display module requires 3-5 different bonding equipment and bonding equipment, and most of the processes need to be tested. Corresponding to 5-6 testing equipment, module production The capacity per million pieces/year corresponds to an investment of approximately 6 million equipment. From this, it can be inferred that in 2017, the global OLED module automation equipment market space will reach 6.19 billion yuan, and the annual market space will reach 82.8/74.03/72.59 billion yuan in 2018/2019/2020.

The 7 billion market space has spawned a billion-dollar market value module automation local enterprise. According to our calculations, the market space of the entire module automation equipment is 7 billion. According to the 25% net interest rate of non-standard automation equipment, we believe that the profit of the whole industry is about 1.8 billion. If the leading company can take 30% of the whole industry. Profit, then we believe that the industry is expected to generate about 15 billion market capitalization of listed companies. From the situation of several mainstream non-standard automation equipment companies, we are optimistic about Zhiyun's leading edge in the Bonding business and the platform integration capability after cutting into the bonding equipment. At the same time, we pay attention to the card position and layout of Jingzheng Electronics, Liande Equipment, Shenkeda and Zhengye Technology in their respective fields.

Risk factor

The capacity and yield of the evaporation equipment are not up to expectations: the evaporation equipment is the lowest yield in the OLED panel manufacturing process, and there is only one supplier that can supply large quantities in a stable manner. Therefore, the evaporation equipment is accelerated to some extent in the industry. A key bottleneck and risk point for development.

The demand for downstream smartphones is slowing down: smartphones are now maturing, the pace of replacement is slowing, and competition is fiercer.

Increased competition in the equipment manufacturing industry: China, Japan and South Korea equipment manufacturers accelerate the pace of research and development and expansion, industry competition has increased risks.

Guangdong Kaihua Electric Appliance Co., Ltd. , https://www.kaihuacable.com