In recent years, computing workloads have been migrating: first from local data centers to the cloud, and now more and more from cloud data centers to "edge" locations closer to the data source being processed. The goal is to improve the performance and reliability of applications and services by shortening the data transmission distance, reduce operating costs, and thereby reduce bandwidth and delay issues.

Is the cloud center "dead"? 10% of traditional data centers closed in 2018

This is not to say that on-premises or cloud centers are dead. Some data always needs to be stored and processed in a centralized location. But the digital infrastructure is definitely changing. For example, according to Gartner, 80% of enterprises will close their traditional data centers by 2025, compared with 10% in 2018. Data processing driven by various business needs is a key driving factor for the development of this infrastructure.

With the recent increase in business-driven IT initiatives (often beyond traditional IT budgets), the implementation of IoT solutions, edge computing environments, and "non-traditional" IT has grown rapidly. In addition, people are paying more and more attention to the customer experience of external applications, and the direct impact of poor customer experience on corporate reputation. This outward focus has led many organizations to reconsider the placement of certain applications based on network latency, customer base clustering, and geopolitical restrictions (for example, the European Union’s General Data Protection Regulation [GDPR] or regulatory restrictions).

Of course, edge computing involves challenges (intermittent) because the edge of the network is characterized by low bandwidth and high latency. If a large number of smart edge devices are running software, such as machine learning applications that need to communicate with a central cloud server or nodes in the middle "fog", this will cause problems. However, the solution is underway.

As edge computing is at the peak of Gartner's cloud computing hype cycle in 2018, there are still many possible errors before standards and best practices are determined, and mainstream adoption can continue. This ZDNet special report aims to assess the current state of competition in a setting scenario. We have edited and organized without changing the original intention:

definition

Edge computing is a relatively new concept that has been associated with another term "fog computing", which may cause confusion among non-professional observers. Here are some definitions that hopefully clarify the situation.

Futurum Research

Unlike cloud computing, which relies on data centers and communication bandwidth to process and analyze data, Edge Computing keeps processing and analysis near the edge of the network where the data was originally collected. Edge computing (a type of fog computing that focuses on network node-level processing and analysis) should be regarded as a factual element of fog computing.

Edge of the Edge 2018

Provide computing power to the edge of the network to improve the performance, operating costs and reliability of applications and services. By shortening the distance between the device and the cloud resources that provide services for it, as well as reducing the number of network hops, edge computing reduces the delay and bandwidth limitations of today's Internet and introduces new application categories. In practice, this means that between today's centralized data centers and more and more equipment, new resources and software stacks will be allocated on the path, especially in terms of infrastructure and equipment near the last mile network.

451 Research / OpenFog Consortium

Fog computing "starts" from one end of the edge device (in this context, we define the edge device as the device from which sensor data is sourced, such as vehicles, manufacturing equipment, and smart medical equipment). These devices have the necessary computing hardware and operating systems , Application software and connections participate in distributed computing. It extends from the edge to "near edge" functions, such as local data centers and other computing assets, multi-access edge (MEC) functions in enterprise or carrier wireless access networks, and intermediate computing and storage functions in managed service providers /Interconnection/Hosting facilities, ultimately to the cloud service provider's services. These locations have integrated or hosted'fog nodes'.

David Linthicum (Chief Cloud Strategy Officer, Deloitte Consulting)

"Edge computing and storage systems are also located at the edge, as close as possible to the components, devices, applications, or people that generate the data being processed. The goal is to eliminate processing delays because the data does not have to be sent from the edge of the network to the central processing system, and then back Edge...The term "fog computing" created by Cisco also refers to extending computing to the edge of the network. Cisco introduced fog computing in January 2014 as a way to bring cloud computing functions to the edge of the network.. .... In essence, fog is the standard, and the edge is the concept. Fog implements a repeatable structure in the concept of edge computing, so enterprises can push computing out of a centralized system or cloud for better and more scalable performance."

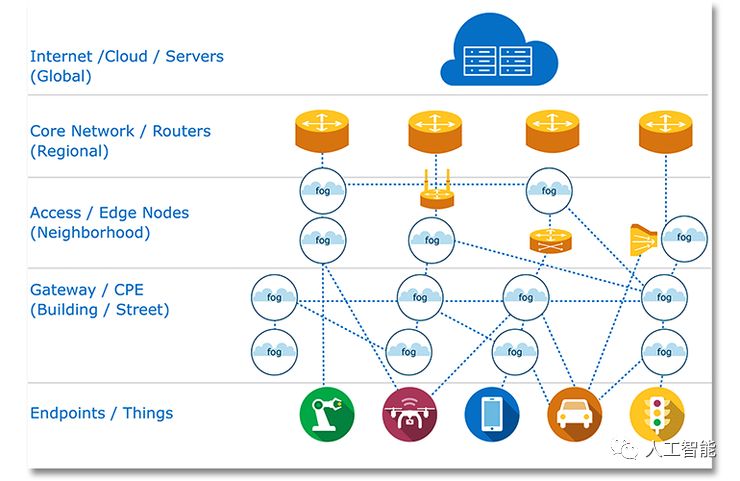

The following is how the OpenFog Alliance visualizes the data generation "things" at the edge of the network, the relationship between the core cloud data center and the fog infrastructure between the two:

Image: OpenFog Consortium

Market estimate

According to data from B2B analyst MarketsandMarkets, by 2022, the value of the edge computing market will reach 6.72 billion U.S. dollars, higher than 2017's 1.47 billion U.S. dollars, with a compound annual growth rate of 35.4%. The key drivers are the emergence of the Internet of Things and 5G networks, the increase in the number of "smart" applications, and the increase in cloud infrastructure load.

Edge computing market dynamics

Among the vertical market segments, telecommunications and IT companies will have the largest market share during the 2017-2022 forecast period. This is because enterprises face high network load and increasing bandwidth requirements, and need to optimize and expand their radio access network (RAN) in order to provide an efficient mobile (or multi-access) edge computing (MEC) environment for their applications and services .

MarketsandMarkets said that during the forecast period, the fastest growing part of the edge computing market is likely to be the retail business: the large amount of data generated by IoT sensors, cameras and beacons can be collected, stored and processed more efficiently at the edge of the network instead of the cloud Or local data center.

Grand View Research takes a more conservative view and estimates that the value of the edge computing market will reach US$3.24 billion by 2025, although this is still an "extraordinary" compound annual growth rate of 41% during the 2017-2025 forecast period. Leifeng.com learned that the research company said that from a regional perspective, North America will lead the market due to the increased penetration of IoT devices in the United States and Canada, and the vertical areas with the highest CAGR will be healthcare and life sciences, which benefits In the "storage capacity and real-time" computing provided by edge computing solutions.†Grand View Research said that because edge computing solutions can reduce operating costs, SMEs will have the highest compound annual growth rate during the forecast period (46.5%) .

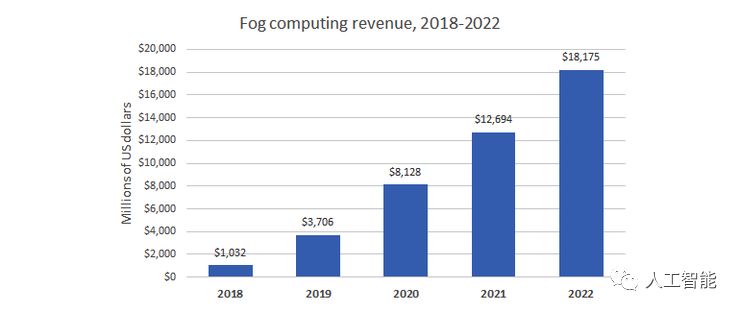

The most optimistic growth forecast comes from 451 Research, "The Size and Impact of the Fog Computing Market" in an October 2017 study (commissioned by OpenFog Consortium). This extensive research brings the market opportunity of atomized computing to 18.2 billion U.S. dollars in 2022, higher than 1.03 billion U.S. dollars in 2018 and 3.7 billion U.S. dollars in 2019, with a compound annual growth rate of 104.9% from 2018 to 2022.

Data: 451 Research & OpenFog Consortium / Chart: ZDNet

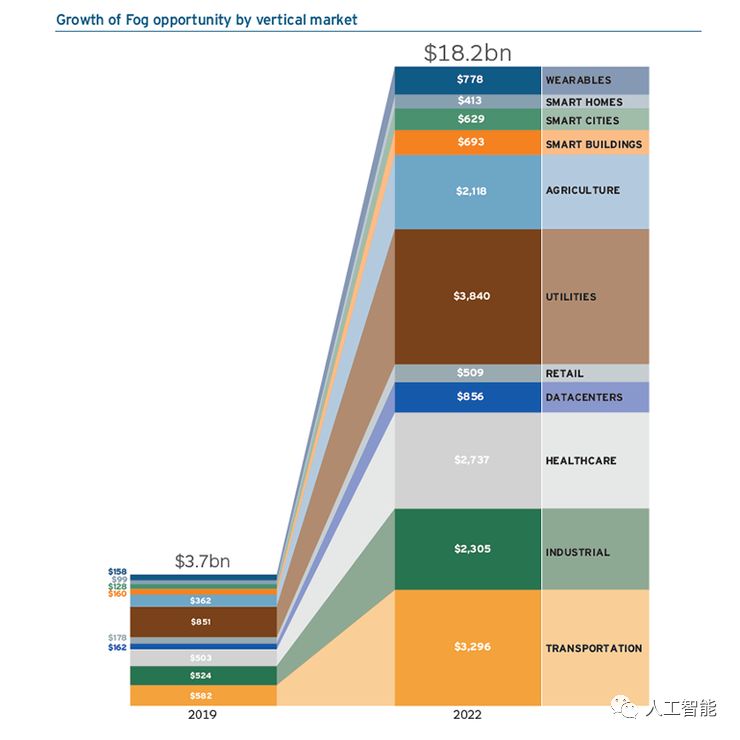

According to 451 Research, in terms of market share, the main vertical industries for fog computing in 2022 will be utilities, transportation, healthcare, industry, and agriculture.

Image source: 451 Research & OpenFog Consortium/ Chart: ZDNet

Speaking of the fog computing ecosystem in 2022, 451 Research has broken down such components: Data: 451 Research & OpenFog Consortium / Chart: ZDNet

Hardware components performed well, accounting for 42.1% in the 2022 pie chart, followed by fog application/platform (21.5%) and fog service (20.4%). No wonder hardware vendors and cloud application/service providers are waiting in line for the fast-growing edge/fog market.

Although they have different focuses, these predictions clearly show that the "perfect storm" of edge computing is being created by the rapidly growing Internet-connected devices and the upcoming high-bandwidth, low-latency 5G network. Ericsson’s June 2018 mobile report summarizes the expected developments in these areas.

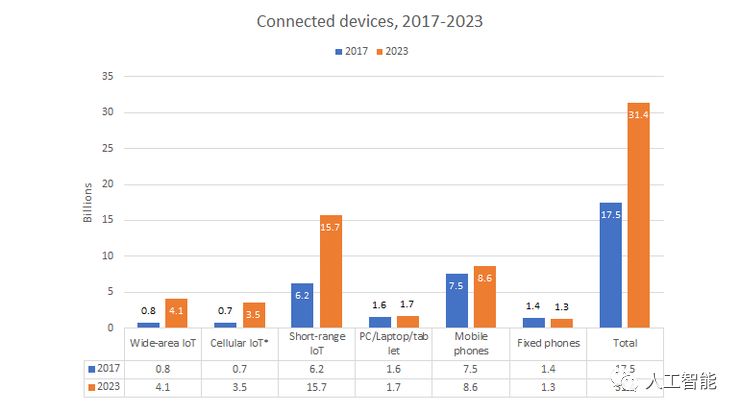

Although personal computers, laptops, tablets, and (to a lesser extent) mobile phones have seen flat growth between 2017 and 2023, IoT devices are taking off: those with wide-area connectivity will achieve 30% annual growth. Compound growth rate, the growth of short-distance IoT devices slowed down (17% compound annual growth rate). This resulted in an increase of nearly 80% (79.4%) in the number of connected devices between 2017 (17.5 billion) and 2023 (31.4 billion).

Cellular IoT devices are a subset of wide-area IoT devices

Data: Ericsson Mobile Report, June 2018/Chart: ZDNet

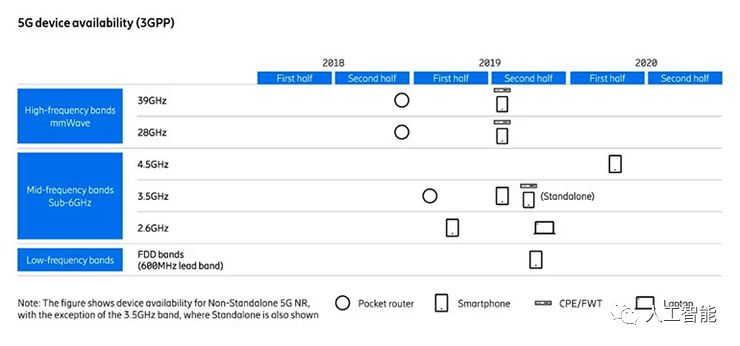

As far as 5G is concerned, Ericsson expects the first batch of data-only devices in the second half of 2018 and the first batch of 5G smartphones in 2019. With the advent of the third-generation chipset in 2020, the company expects that 1 billion 5G devices will be connected worldwide by 2023.

CPE / FWT: Customer-supplied equipment/fixed wireless terminal

Picture: Ericsson Mobile Report, June 2018

Ericsson said that the first module-based 5G IoT devices are expected to support ultra-low latency communications for industrial process monitoring in 2020.

Standards and organizations for edge computing

Any new IT plan requires standards and best practices, and the early stages usually consist of multiple groups and alliances with different agendas (although there are often significant differences in membership). Edge/fog computing is no exception.

Fog computing is a term coined by Cisco and supported by the OpenFog Consortium, which was established in 2015 by Arm, Cisco, Dell, Intel, Microsoft and Princeton University Edge Lab. The mission statement (part of) is as follows:

Our work will define the architecture of distributed computing, network, storage, control, and resources to support intelligence at the edge of the Internet of Things, including self-aware machines, objects, devices, and smart objects. OpenFog members will also identify and develop new operating models. Ultimately, our work will help realize and promote the next generation of the Internet of Things.

Edge computing is promoted by EdgeX Foundry, an open source project hosted by the Linux Foundation. The goals of EdgeX Foundry include: building and promoting EdgeX as a universal platform for unified IoT edge computing; certifying EdgeX components to ensure interoperability and compatibility; providing tools to quickly create EdgeX-based IoT edge solutions, and related Open source projects, standards organizations and industry alliances cooperate.

According to EdgeX Foundry, "The best point of this project is the edge nodes, such as embedded PCs, hubs, gateways, routers and local servers, to solve the key interoperability of the interaction of the'east, west, south, north' in the distributed IoT fog Challenge architecture."

EdgeX Foundry's technical steering committee includes representatives from IOTech, ADI, Mainflux, Dell, Linux Foundation, Samsung Electronics, VMWare and Canonical.

There are two other industry organizations in this field: Japan’s focused EdgeCross Alliance, which was established in November 2017 by Omron Corporation, Advantech, NEC, IBM Japan, Oracle Japan, and Mitsubishi Electric; and the Industrial Internet Alliance, which was formed by AT&T, Cisco, and General Electric. , Intel and IBM were established in 2014.

Edge Computing Index: From Edge to Enterprise

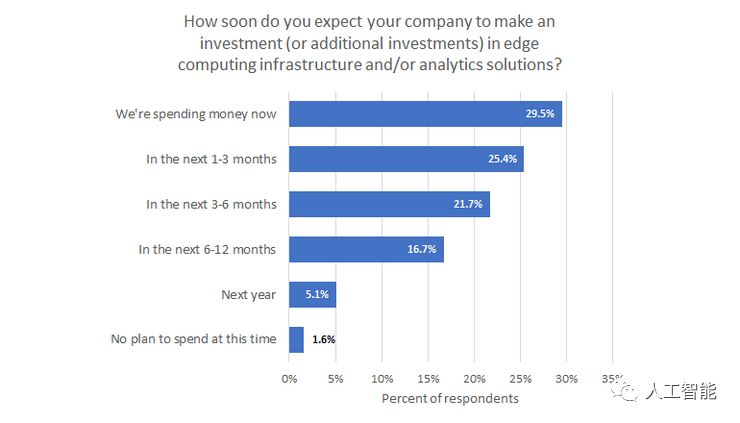

Futurum Research conducted a survey of more than 500 North American companies (ranging from 500 to 50,000 employees) at the end of 2017 to discover their solution adoption and deployment, investment intentions, etc. in edge computing. Futurum stated that all interviewees had an impact on edge computing investment decisions, of which 41.8% were "operations" and 25.6% were "directors, managers, team leaders"; but only 8.6% were classified as " Executives, senior managers, owners, partners".

Futurum reports that nearly three-quarters (72.7%) of companies have implemented or are implementing an edge computing strategy. In addition, almost everyone (93.3%) intends to invest in edge computing in the next 12 months.

Data: Futurum Research / Chart: ZDNet

Futurum also curated a universal digital transformation index that included 68% of companies in the "leader" and "adopter" categories in 2018. Therefore, 72.7% of respondents have invested in edge computing, which shows that this is a hot topic for technology-savvy companies. However, Futurum also pointed out that "93.3% of enterprises' enthusiasm for investing in edge computing in the next 12 months is not on par with the scale of their investment."

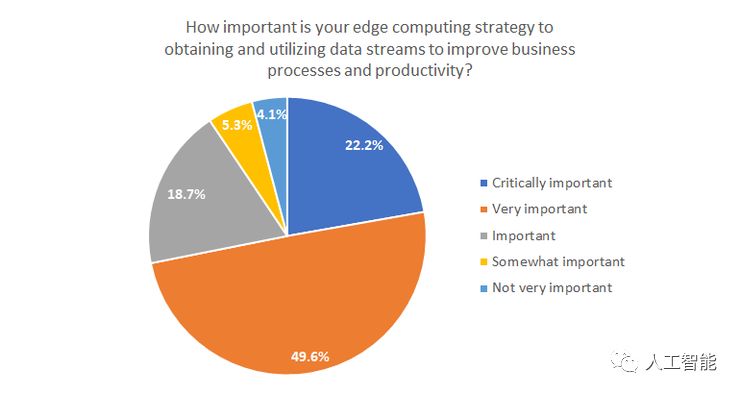

When asked about the importance of edge computing data flow in their business processes, the positive atmosphere among Futurum respondents continued, with 71.8% of respondents describing it as "extremely" (22.2%) or "Very" (49.6%) important:

Data: Futurum Research / Chart: ZDNet

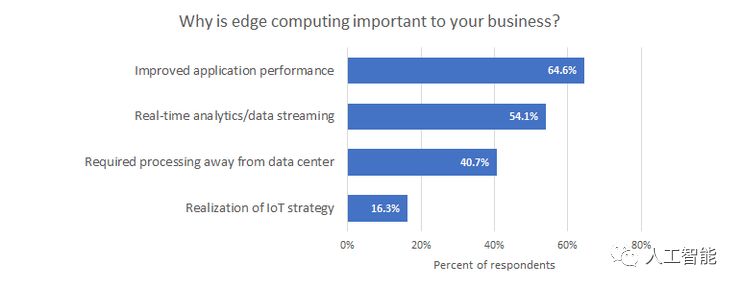

What are the key drivers of this enthusiasm for edge computing? For Futurum respondents, it is "improved application performance", followed by "real-time analysis/data streaming":

Data: Futurum Research / Chart: ZDNet

The analysis company interprets these priorities as a reflection of the need for operational efficiency, indicating that the IoT strategy ranks relatively low, often referred to as standardized edge computing use cases, and "may increase in the next few years."

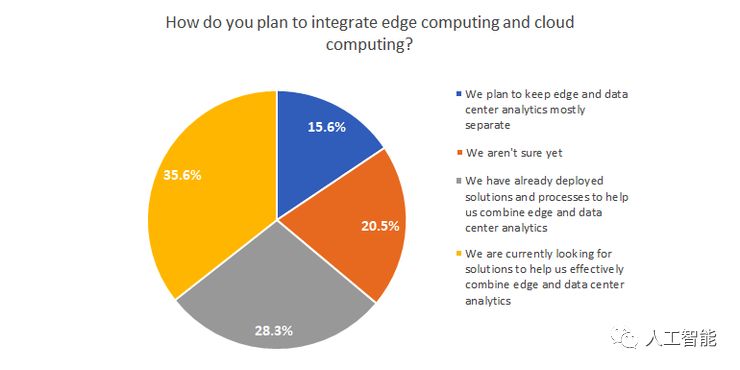

The research firm said that only 15.6% of Futurum respondents aimed to separate edge computing from cloud computing. This decision is usually driven by data and system security issues and focuses on partitioned operations. This makes nearly 64% (63.9%) have deployed (28.3%) or are seeking (35.6%) edge/data center analytics solutions, plus 20.5% are unsure whether to combine these functions or separate them:

Data: Futurum Research / Chart: ZDNet

"Uncertain" and "seeking a response" accounted for 56.1% of the survey sample, which is obviously an important opportunity for edge computing providers.

2018 fog computing outlook

In December 2017, OpenFog Consortium conducted a survey on the fog computing status of its 61 member organizations, and found that it is impressive that 70% of CEOs are aware of the fog computing changes they have seen.

In 2018, the fog computing budget generally increased (40%) or remained the same (51%), and only 5% of the respondents felt it was reduced. The initiative is mainly based on the R&D department (51%), and most of them focus on IoT applications (70%).

Security is the number one concern among OpenFog respondents (32%), followed by concerns about early/unproven technology, interoperability and unclear return on investment. The main driving factors of fog computing are latency and bandwidth issues. Respondents expect manufacturing, smart cities, and transportation to be the top industries using fog computing, followed by energy, healthcare, and smart homes.

Main supplier

Edge/fog computing can pull workloads away from cloud data centers, so it's not surprising to see cloud giants taking steps to prevent these workloads from escaping their tracks.

Amazon AWS

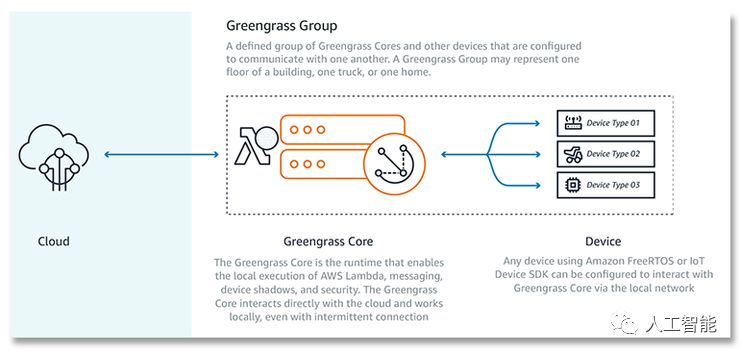

Leifeng.com learned that at Amazon's 2016 re:Invent Developer Conference, AWS Greengrass will expand AWS to intermittently connected edge devices based on the company's existing IoT and Lambda (serverless computing) products.

"With AWS Greengrass, developers can add AWS Lambda functions to connected devices directly from the AWS management console, and the device can execute code locally so that the device can respond to events and perform operations in near real time. AWS Greengrass also includes AWS The IoT messaging and synchronization capabilities allow devices to send messages to other devices without connecting back to the cloud.†Amazon also said, “AWS Greengrass allows customers the flexibility to make devices rely on the cloud when it makes sense. Performing tasks on your own when you are, and talking to each other when it makes sense, all of this is done in a seamless environment."

AWS-greengrass

Of course, these are "smart" edge devices: Greengrass requires at least 1GHz of computing (Arm or x86), 128MB of RAM, and additional resources for the operating system, message throughput, and AWS Lambda execution. According to Amazon, "Greengrass Core can run on a variety of devices from Raspberry Pi to server-level devices."

Microsoft

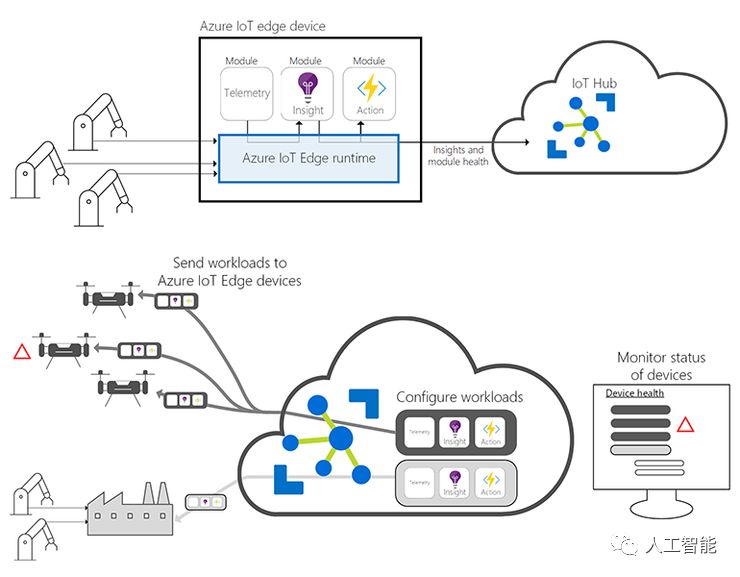

Since June 2017, Azure IoT Edge has been launched at Microsoft's BUILD 2017 Developer Conference, allowing cloud workloads to be containerized and run locally on smart devices ranging from Raspberry Pi to industrial gateways.

Azure IoT Edge includes three components: IoT Edge module, IoT Edge runtime environment, and IoT center. IoT Edge modules are containers that run Azure services, third-party services, or custom code; they are deployed to IoT Edge devices and executed locally. The IoT Edge runtime environment runs on each IoT Edge device and manages the deployed modules, while IoT Hub is a cloud-based interface for remote monitoring and management of IoT Edge devices.

Here is how the different Azure IoT Edge elements fit together:

Azure-IOT-edge

With the full listing, Microsoft has added new features, taking Azure IoT Edge as an example, including: open source support; backup configuration, security and management services, and simplified developer experience.

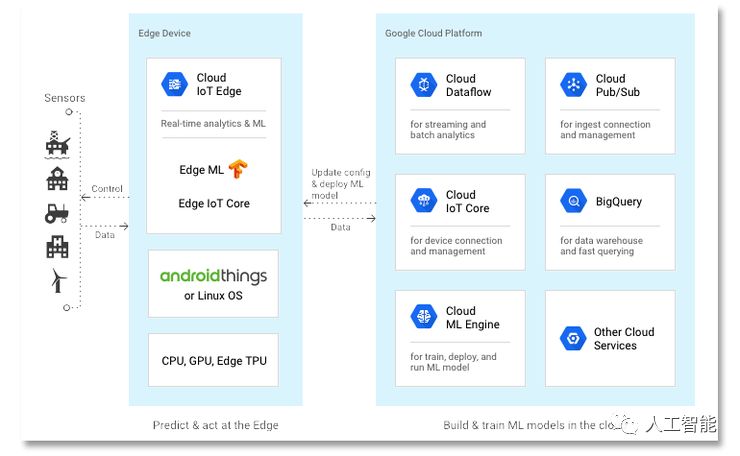

In July 2018, Google announced the launch of two products for large-scale development and deployment of smart connected devices: Edge TPU and Cloud IoT Edge. Edge TPU is a special small ASIC chip designed to run TensorFlow Lite machine learning models on edge devices. Cloud IoT Edge is a software stack that extends Google's cloud services to IoT gateways and edge devices.

Cloud IoT Edge has three main components: it is used for the runtime of gateway-level devices (with at least one CPU), used for storage, conversion, processing, and extraction of intelligence from edge data, while interoperating with Google's other cloud IoT platforms; The Edge IoT Core runtime can safely connect edge devices to the cloud; the Edge ML runtime is based on TensorFlow Lite and uses a pre-trained model to perform machine learning inference.

Google Cloud-IOT-edge

At the time of writing (September 2018), Edge TPU and Cloud IoT Edge are both in alpha testing.

Concluding remarks

The edge/fog calculation conversion is one of the focus shifts that occur regularly in calculations. For example, from mainframes to desktop PCs, to local data centers, and then to cloud data centers. Now, we are studying the mix of existing elements, and billions of smart IoT devices, which are connected by the "fog" between gateways and nodes. Device connection has always been the bottleneck hindering this transition, but with the emergence of 5G mobile networks, this situation is about to change dramatically.

Any industry sector that can benefit from timely analysis of IoT data streams will be interested in edge/fog computing. This is why there are huge opportunities for vendors at all levels of the technology stack.

As more and more data is generated, processed, and stored in more locations, issues surrounding infrastructure management and data security, privacy, and governance will become more important than they are now. Let us hope that these issues will be resolved as soon as possible.

Guangzhou Yunge Tianhong Electronic Technology Co., Ltd , https://www.e-cigarettesfactory.com